Lack of Credit Strategy From the Beginning 🚫

Many startups fail because credit planning is treated as an afterthought rather than a foundational business decision. Entrepreneurs often focus heavily on product development, branding, and customer acquisition while ignoring how their business will access and manage credit. Without a clear strategy, startups rely on personal credit cards or short‑term borrowing, which quickly becomes unsustainable. Poor planning leads to reactive decisions instead of proactive financial control. When unexpected expenses arise—as they always do—businesses without established credit lines struggle to cover costs. This lack of foresight limits growth opportunities and increases financial stress, often forcing startups into high‑interest debt or premature shutdowns.

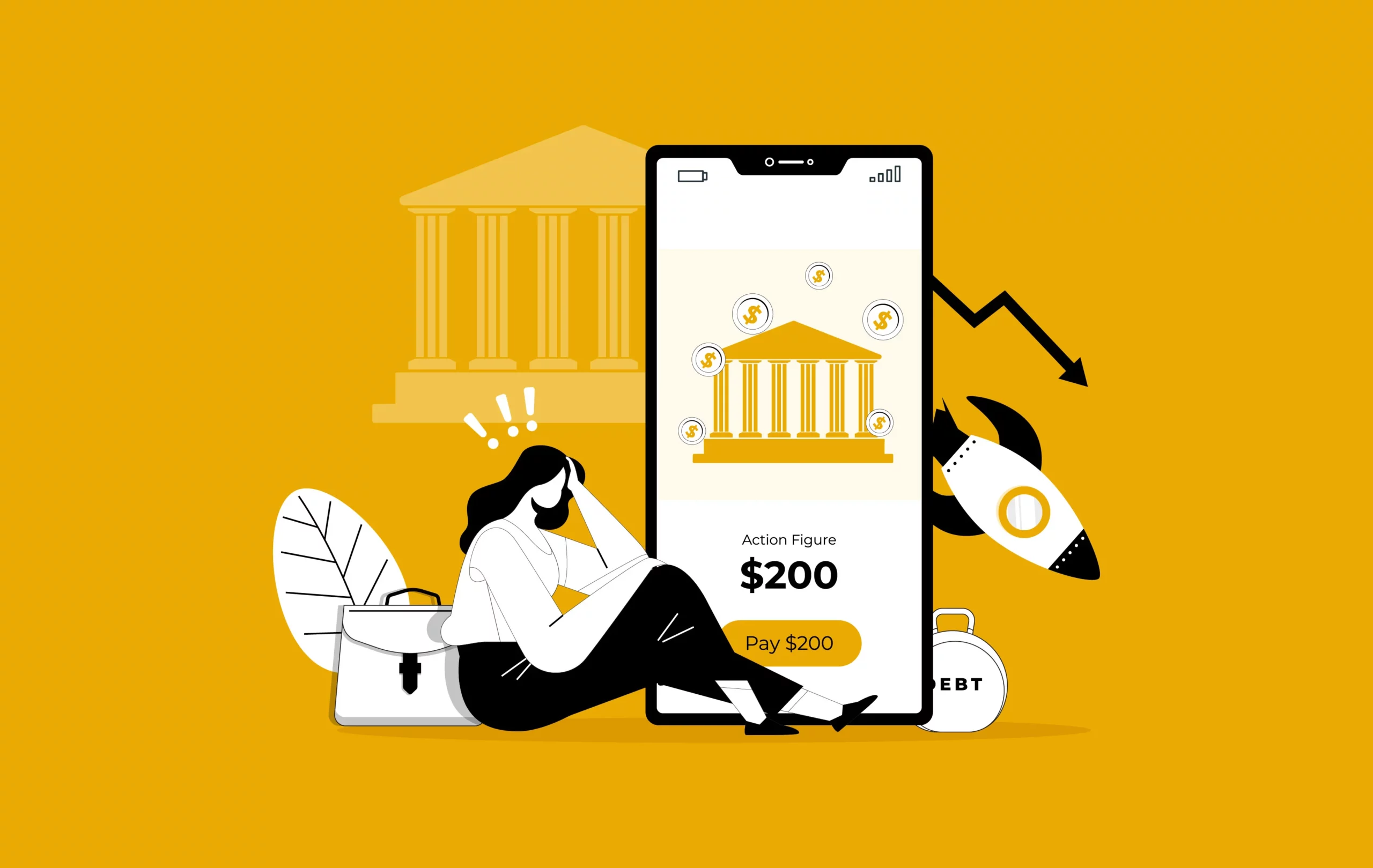

Overreliance on Personal Credit Creates Risk 💳

One of the most common mistakes new founders make is using personal credit to finance business operations. While this may be convenient early on, it creates serious long‑term risk. High utilization on personal cards lowers personal credit scores, making future financing harder to obtain. If the business struggles or fails, the personal financial fallout can be devastating. Additionally, lenders often view startups that rely heavily on personal credit as unstable. This dependency blurs the line between personal and business finances, making the company appear unprofessional and financially unprepared. Over time, this approach limits access to legitimate business funding and increases the likelihood of failure.

Inability to Qualify for Funding When It’s Needed Most 🏦

Startups often need financing at critical growth stages—such as hiring staff, purchasing inventory, or scaling operations. Poor credit planning makes it difficult to qualify for loans, lines of credit, or favorable vendor terms at these moments. Without a solid credit foundation, lenders see startups as high risk and either deny applications or offer funding at extremely high interest rates. Missed financing opportunities slow growth and allow competitors to gain an advantage. In many cases, startups collapse simply because they cannot access capital when it matters most, even if the business model itself is strong.

Cash Flow Problems Escalate Without Credit Buffer 💸

Healthy cash flow is essential for survival, and proper credit planning acts as a buffer when revenue fluctuates. Startups without credit planning often operate with razor‑thin margins and no safety net. Delayed client payments, seasonal sales dips, or unexpected expenses can quickly push the business into crisis. Without access to credit, founders are forced to delay payments, miss payroll, or halt operations altogether. Poor cash flow management combined with no credit backup creates a domino effect that leads to missed obligations, damaged vendor relationships, and reputational harm. These cash flow breakdowns are a leading cause of early startup failure.

High-Interest Debt Drains Growth Potential 📉

When credit planning is ignored, startups often turn to last‑resort financing options such as payday loans, merchant cash advances, or unsecured high‑APR credit cards. These products come with aggressive repayment terms that drain revenue before it can be reinvested into growth. High interest payments reduce profitability and create constant financial pressure. Instead of using earnings to build the business, founders are stuck servicing debt. This trap limits innovation, slows hiring, and makes long‑term sustainability nearly impossible. Smart credit planning helps startups access lower‑cost financing options that support growth instead of suffocating it.

Vendor Trust and Business Reputation Suffer ⚠️

Vendors, suppliers, and partners often evaluate a startup’s creditworthiness before extending payment terms or entering long‑term agreements. Poor credit planning leads to missed payments, inconsistent billing behavior, or demands for upfront cash only. These red flags damage trust and force startups to operate under less favorable conditions. Without Net‑30 or Net‑60 terms, cash flow becomes even tighter. A weak credit profile also reduces negotiating power, leading to higher costs and limited supplier options. Reputation is everything for a startup, and credit behavior plays a major role in how reliable and professional a company is perceived.

Failure to Separate Business Credit Limits Growth 🚀

Startups that never establish business credit remain permanently tied to the founder’s personal financial profile. This limits scalability and makes it difficult to transition into larger funding, partnerships, or acquisitions. Investors and lenders prefer businesses with independent credit histories because it signals stability, structure, and long‑term viability. Without business credit, startups struggle to qualify for corporate cards, equipment financing, commercial leases, or expansion capital. This lack of separation keeps the business small and fragile. Proper credit planning allows startups to grow beyond the founder’s personal limits and build a foundation capable of supporting long‑term success.